High-level employees and executives at publicly traded companies often accumulate substantial wealth tied up in company stock through RSUs, stock options, or ESPPs. These holdings can quietly grow to represent 20%, 30%, or more of their liquid net worth over time. While this concentration signals success, it creates unique portfolio risks, particularly when a single company’s stock dominates retirement plans and net worth.

Diversifying away from a concentrated position, especially one with significant embedded capital gains, is typically easier said than done. Immediate sales often trigger large tax bills, and the emotional and political dynamics around company stock can cause hesitation or delays. However, there is an emerging strategy high-net-worth investors can utilize to diversify in a tax-neutral manner.

Enter Long/Short Loss Harvesting

A powerful, tax-efficient diversification strategy gaining traction is called long/short loss harvesting. Instead of selling all or a chunk of the concentrated stock outright and realizing potentially hefty capital gains taxes, investors transfer that appreciated stock into an account managed with a long/short approach. The manager enhances the concentrated stock position by acquiring additional securities using leverage, while simultaneously establishing a short position by selling borrowed securities.

How the Long/Short Strategy Works

In simple terms, the manager implements a long portfolio that benefits from upward movements in stocks while simultaneously maintaining a short portfolio that profits when the market falters. This approach means an investor can realize capital losses independent of the environment. If the market rises, they can recycle their short positions and if stocks decline, they have their new longs to tax manage.

This increased opportunity to realize losses allows investors to use the harvested losses to offset the capital gains embedded in the concentrated stock over time. It’s a unique approach that can save investors a significant amount of tax!

Real-Life Example: Diversifying $5 Million in Apple Stock with Long/Short Loss Harvesting

Consider James who holds approximately $5 million of Apple (AAPL) stock purchased in the 1980s for a few thousand dollars (0.1% of the market value). He is becoming concerned about his concentration but is hesitant to sell given the large gain. Previously and without an alternative, that would be the end of the conversation, but with long/short loss harvesting we have an opportunity to tax-efficiently diversify overtime.

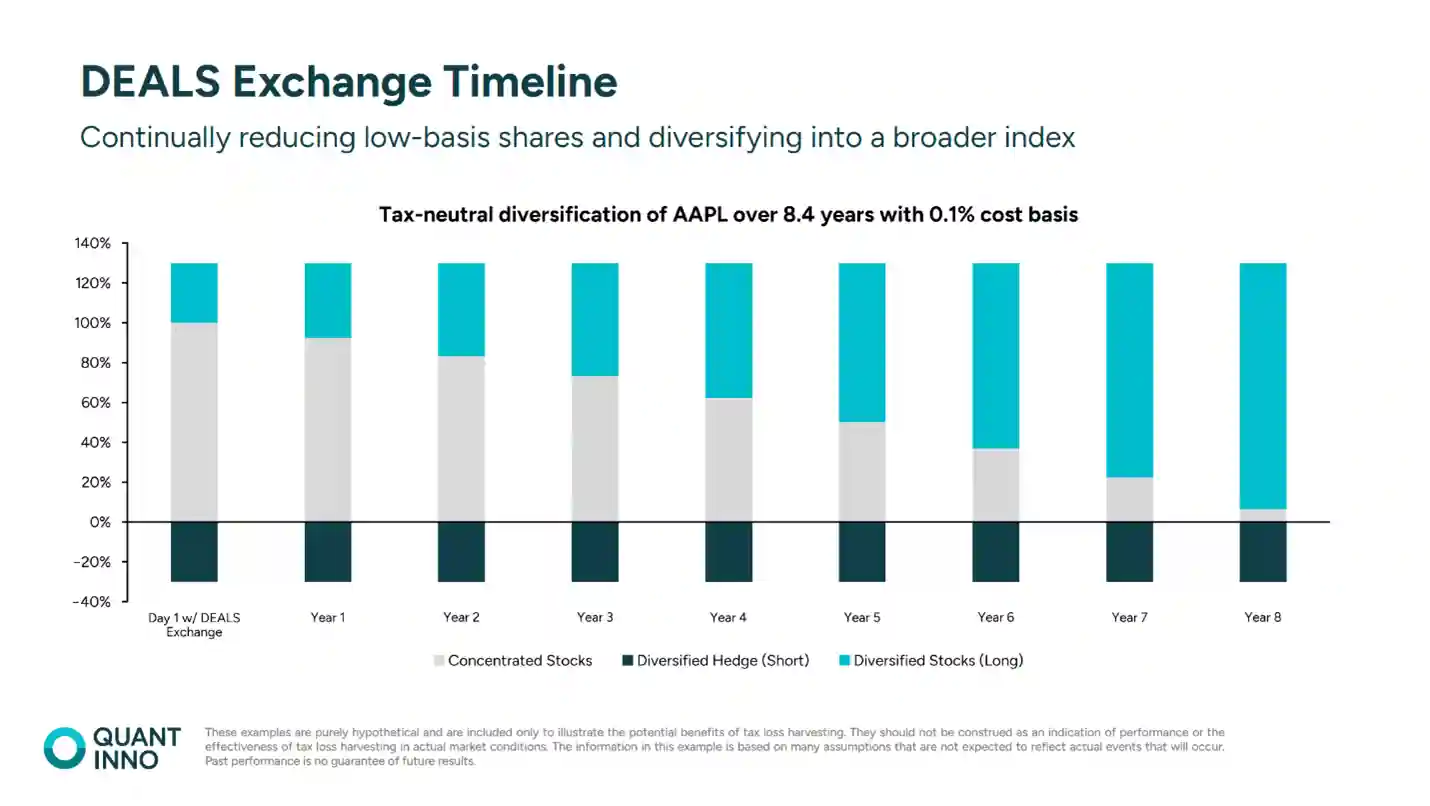

By implementing the 130/30 strategy (160% gross exposure = 100% long core, 30% long extension, 30% short extension), James can achieve tax-neutral diversification of the concentrated APPL over approximately 8.5 years. This timeline reflects the gradual sale of shares as losses are realized in the non-AAPL position.

Compare this to simply selling the stock over 8.5 years, a $5 million capital gain spread over that period means James would realize ~$588,000 of long-term capital gain each year. He would be paying ~$140,000 in federal capital gains each year. This is a total game changer for James, he thought he would have to keep his AAPL stock forever, but not anymore.

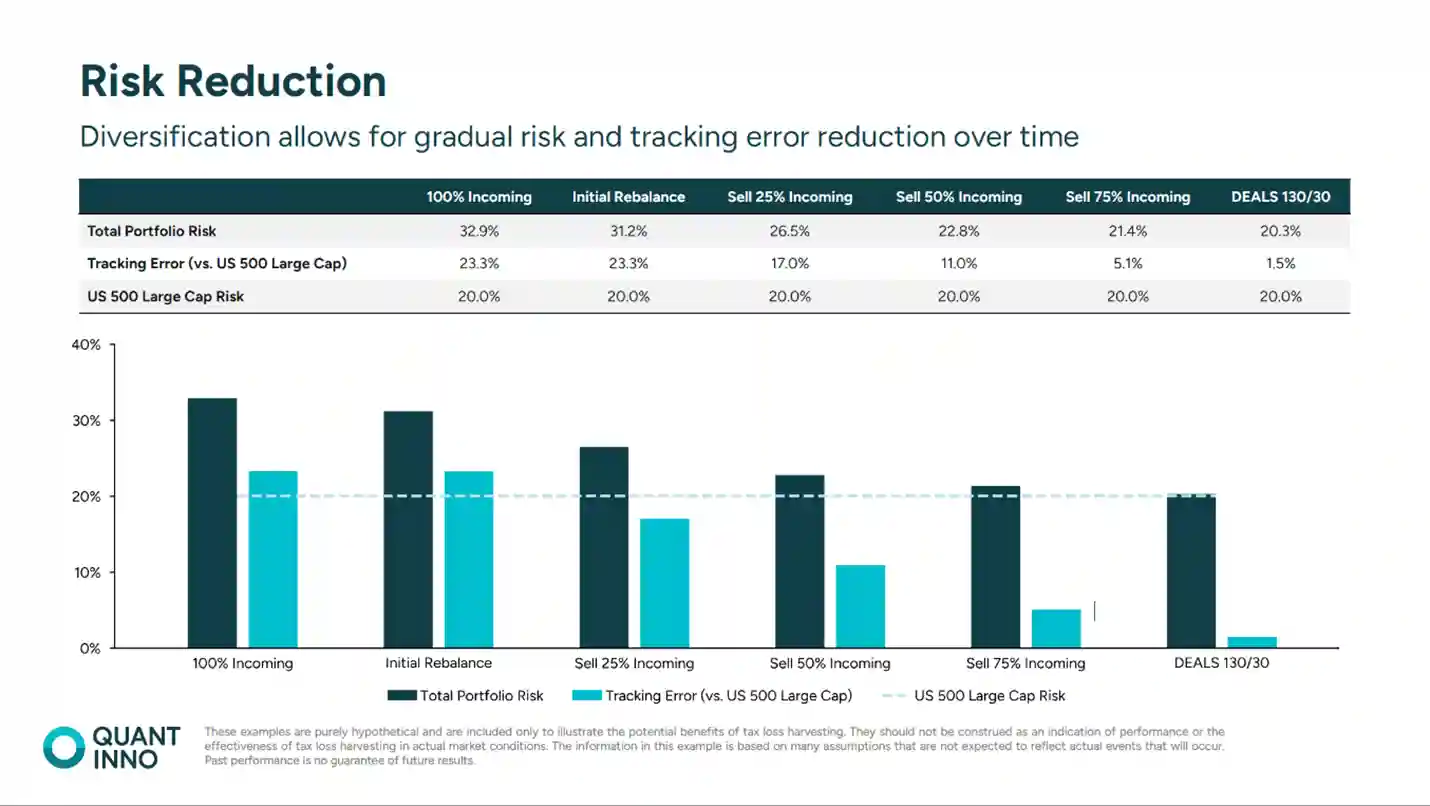

In addition to the tax savings, as James steadily sells down AAPL, proceeds are invested into a diversified portfolio which means he is lowering his risk and tracking error to the benchmark.

This example illustrates how a long/short loss harvesting strategy can facilitate a multi-year, tax-efficient plan to diversify out of a concentrated, low-cost-basis stock position.

Practical Considerations & Risks

- Complexity: Long/short loss harvesting requires sophisticated portfolio construction, margin management, and tax-aware trading algorithms. This complexity necessitates working with experienced wealth managers who have a track record in managing wash sales, tracking error, and other nuances.

- Costs: There are added costs from leverage, short rebate spreads, and higher management fees relative to long-only indexing. These should be carefully weighed against tax alpha and diversification benefits.

- Wash Sale Rule: The IRS wash sale rule prohibits claiming a loss if a substantially identical security is repurchased within 30 days before or after a sale. Effective long/short loss harvesting programs use nuanced substitution strategies to comply with these rules while maximizing loss capture.

Conclusion

For high-net-worth executives with significant wealth tied up in company stock, long/short loss harvesting is transforming how investors think about diversification. Instead of surrendering to capital gains taxes or remaining over concentrated in a single stock, this strategy unlocks a path to gradual, tax-neutral diversification. By systematically capturing losses and reinvesting proceeds into a diversified portfolio, investors can protect their success while building resilience for the future. If you’re holding a large single-stock position with embedded gains, now is the time to explore your options. To learn more about this strategy and how it applies to your portfolio, contact us today.